Dine Brands ($DIN): How cheap is too cheap?

The franchisor of Applebee's and IHOP trades at 5x earnings.

Executive Summary

Dine Brands is the kind of business that makes analysts groan. Their brands are unexciting, their business performance is unimpressive, and their management is uninspiring. But the asset-light business is likely to throw off a steady $80m/yr in owner earnings for the foreseeable future.

How much would such a business be worth to a private owner? With the 10-year at 4.4%, I’d say no less than $800 million, and potentially a fair bit more. But right now, the US stock market only has eyes for growth — and that means you can pick up shares at a valuation of only $400m.

Granted, it’s not all good news. The current CEO seems to have a bit more of an expansionary tilt than predecessors, and the debt load, while very manageable, is not small. But at the end of the day, we’re looking at a 20% owner earnings yield on a franchise business. A lot has to go wrong for that to go tits-up.

Business Overview

As mentioned, Dine is the franchisor for Applebee’s and IHOP, two US restaurant chains. I’d guess most of my readers are Americans, but for the rest of the world, Applebee’s is a full-service casual dining restaurant, akin to Chili’s or Olive Garden; and IHOP is a 24-hour breakfast chain, similar to Denny’s and somewhat upmarket from Waffle House.

(They also bought a taco shop chain called Fuzzy’s in early 2023, but it’s only ~3% of franchise revenue so fairly immaterial.)

Both Applebee’s and IHOP are pretty much 100% franchised, with 97% of those franchises being in the US. Franchisees pay a royalty fee to Dine — 4% of sales at Applebee’s, 4.5% at IHOP; plus an advertising contribution — 3.25% of revenue at Applebee’s, 3% at IHOP. That second fee is rolled straight into ads by Dine, meaning it’s best ignored when looking at the financials — any income statement numbers I quote will be ex-advertising. The royalty fee currently rakes in about $400m per year.

Franchising COGS is only ~10% of revenue, pertaining mostly to a few items at IHOP such as the pancake mix that are produced centrally and sold to franchisees or supermarkets, as well as bad debt expense from lending to franchisees. This leaves ~$360m of franchising gross profit.

There is also the rental segment — Dine owns or leases the real estate for about a third of their IHOP units, which they rent out to the franchisee. This is a hangover from the pre-2003 business model of developing new locations centrally. It brings in about $120m of revenue and $30m of gross profit

Corporate overheads eat up about half of that $390m of overall GP. This includes the salaries of Dine’s 600 employees, who are involved in franchise support, marketing, consumer research, food development, HR and so on; as well as software expenses, professional fees (ugh) and management compensation.

The rest is operating profit. So a pretty healthy margin there — almost 40% of revenue converts.

Growth (or lack thereof)

Absent any changes in fee structure, Dine’s revenue growth rate is simply restaurant count growth + YoY same-store sales (SSS) growth. Taking these one at a time:

Restaurant Count

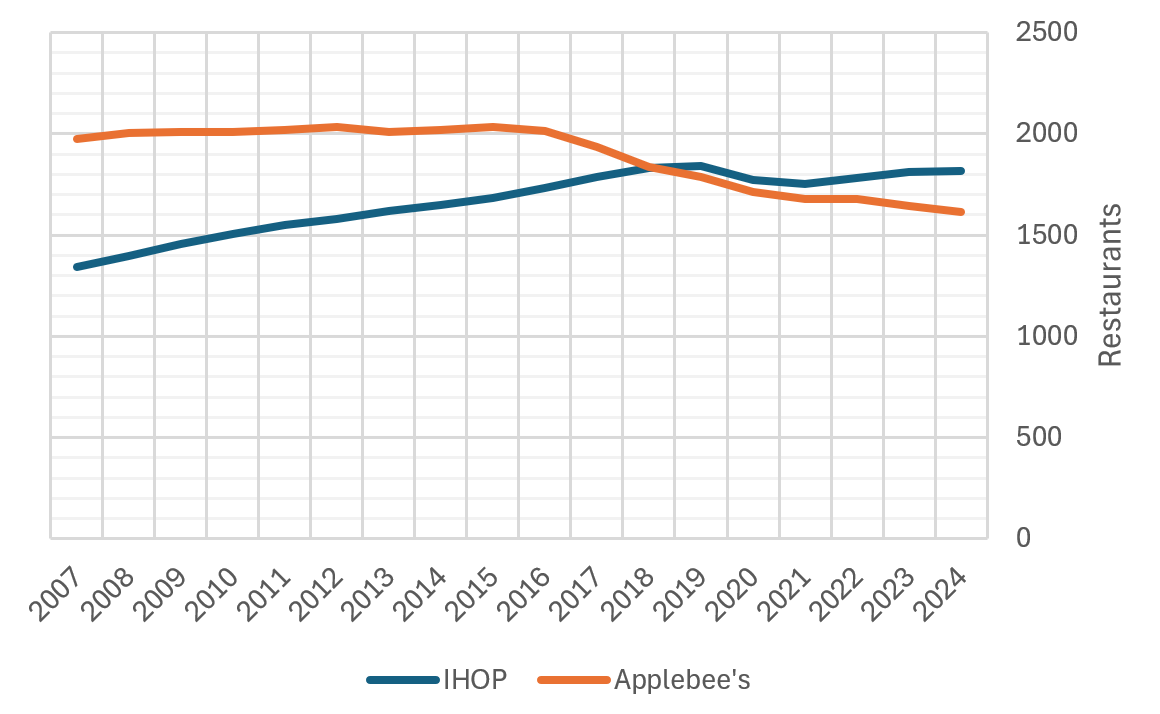

IHOP, in my view, should continue to be a slow grower - the last 5 years look pretty much flat, but covid took a bunch of restaurants out, and 2024 has been an unusually tough year for casual dining restaurants. I think 1-2% annual growth moving forward is a reasonable, conservative assumption (pre-covid, they averaged ~3%).

Applebee’s, on the other hand, is clearly in decline. Between 2016-2021, they lost almost 70 restaurants per year (though covid can be blamed for some of these). However, it has somewhat levelled off since, with net closures of only 72 since 2021. I’m inclined to believe the franchise will lose ~1% of restaurants (15-20) per year, absent a major recession. Management are confident Applebee’s can return to consistent unit growth — but I’ll let that be a happy little surprise on the off-chance it does occur.

Same-Store Sales

SSS is, in turn, a function of traffic and average cheque (check, for the Americans). Unfortunately, Dine does not break its SSS change into those components in reports - but in any case, the numbers aren’t pretty.

These numbers are not inflation-adjusted. Per-store revenues have been almost flat since 2008 - specifically, +9.5% for IHOP and -0.2% for Applebee’s. Literally just keeping up with inflation would have resulted in +46%.

Where does SSS go in the future? I really don’t know. It’s the biggest source of uncertainty in valuing Dine, which is why markets seem focus so single-mindedly on this figure when earnings reports come out. I think the only assumption that can be considered conservative here is zero growth.

Dual-branded restaurants

Here’s a thought. Applebee’s is very much a brunch-afternoon-evening place, which is generally closed during the early morning, and doesn’t receive much traffic in the late evening. On the other hand, IHOP’s fortés are the early morning and late-night crowds — and most locations stay open 24/7. The two brands’ traffic patterns are almost exact opposites.

So… what if you combined the two restaurants into one? You could serve twice as many customers with only slightly more kitchen space (much of the equipment is common across the two) and little to no extra floor space. In an industry with margins as thin as restaurants’, the cost savings there could have a huge impact on the bottom line.

To be clear, this isn’t my idea. In fact, management are already trying it out — 13 dual-branded restaurants are now up and running in international locations (they’re being careful not to freak out the precious US consumer and damage one or both of the brands). Results so far show such locations see 50-100% higher revenue than normal ones — though the effect on build-out costs and margins has not yet been revealed, likely because there aren’t enough normal restaurants in each of those countries to be able to isolate the difference.

However, just a few days ago, the first dual-branded restaurant in the US opened in Seguin, Texas. This location will serve as a key litmus test for the concept — does the average US Applebee’s patron mind having the IHOP riff-raff dining next to them, and vice versa? If the answer is no, I think this could actually be pretty big for Dine. There is already good demand from franchisees — several have already approached the franchisor and expressed their interest in adding the other brand to their existing restaurants, and Dine now has 15 sites lined up for implementation if Seguin is a success. Assuming the unit economics work (and I suspect they do), Dine would likely see a step change in store count growth in this scenario, and over time it would start positively affecting same-store sales too. However, all this depends on the customer reacting well to the concept — and on that question, I am far less sure. So I’m viewing this as just one of a number of possible catalysts that could cause a re-rating — a free call option, if you like.

Management

Things take something of a turn for the worse here. Management are my biggest hang-up with this company.

The CEO is John Peyton. He took the role in 2021 as an external hire, and is two of my least favourite kinds of CEO in one: ex-consulting and ex-marketing. That being said, ex-marketing is pretty common for franchise CEOs, as marketing is really the biggest service they provide to franchisees (check the 1Y chart of $EAT to see what happens when they get it right — more on this later).

He comes across as pretty unremarkable on earnings calls. More corporate than candid, for sure — likes to blame the macro for the business’s poor performance, rather than taking any responsibility. And the business’s performance has been pretty mediocre under his tenure. The stock market is of course a very imperfect indicator, but it’s not insignificant that shares are down well over 50% since he joined 4 years ago.

I also think management are grossly overpaid. Peyton’s 2023 target comp was $6m, with a maximum of almost $9m available. The 4 other execs had a collective target comp of $7.4m, and the directors pull in over $2m collectively too. Altogether, that would be over $15m if they hit targets, for a company earning only ~$110m before comp. The worst bit is, they also spend extra money hiring a “compensation consulting” firm called Exequity, just to tell the board that handing 3.5% of the company to the execs every year for subpar performance is fucking dandy. (Pardon my language — this kind of corporate bullshittery just pisses me off immensely.)

But the most important thing to consider in Dine’s case is probably capital allocation.

What we want from a mature business like this is a solid record of returning the majority of cash to shareholders, only putting cash towards expansion or acquisition when the prospective returns are unusually attractive.

The long-term record looks good from that perspective - more than 80% of FCF generated since 2010 has been returned to shareholders as dividends or buybacks. However, that ratio has fallen to just 39% in 2024, as they’ve pulled back on both dividends (which I’m fine with, as I think they’re a pretty inefficient tool), and share buybacks (which I’m less fine with, given the current valuation). In fact, the company seems to have a history of poor timing with buybacks:

I’m particularly disappointed in the drop to 0 in Q3’24, just as the stock literally reached the lowest level since the GFC, setting aside a few days in March 2020. That’s pretty unjustifiable.

I think we’re also seeing a more expansionary tilt with Peyton than his predecessors. Check out the change in language in their “Strategic Priorities” statement:

2017: "We are focused on generating strong adjusted free cash flow and returning a substantial portion of it to stockholders"

2023: "We will focus on capital allocation strategies to maximize long-term stockholder return, including cash dividends and repurchases of our common stock taking into consideration market conditions. Furthermore, we will continue to evaluate the addition of new brands to our restaurant portfolio through acquisitions and other strategic investments.”

There was also the 2023 acquisition of Fuzzy’s for $80m. It’s pretty clear this was just an attempt to add a bit of a growth story, a little bit of sex appeal to tempt investors, given they paid double the gross profit multiple that they could have then bought their own stock at. It may have worked, was it not for the fact that Fuzzy has seen both store count and same-store sales drop since the purchase.

There may yet be a light at the end of the tunnel. Wedbush analyst Nick Seytan suggested in November that a $100m accelerated share repurchase plan seems like a possibility, explaining:

“We came away from our meetings with CFO Vance Chang and SVP, Finance & IR, Matt Lee incrementally more confident that […] the probability of a meaningful buyback with the >$100M of excess cash on the balance sheet and ongoing ~ $100M annual FCF generation is high.”

I think that’s optimistic. But I also suspect Peyton is receiving a fair bit of pressure from shareholders to repurchase more shares, so we’ll see. My guess for 2025 would be closer to half of this number, but I’m happy taking the possibility of a ~$100m buyback as another free call option.

Financials

Operating

Note that’s EBITA there, not EBITDA. Just EBIT without the meaningless amortization of acquired intangibles charge. I’ll call it operating profit hereafter. I’ve also ignored any goodwill impairment charges and similar.

What are the main takeaways?

Post-covid, the business seems to be capable of earning about £190-200m of operating profit, with very good stability.

SG&A expense increases in-line with inflation. 144 → 195 is a 35% increase, which happens to be the exact CPI increase since 2013 (though there will have been some incremental overheads from buying Fuzzy’s). That might start being a problem if same-store sales don’t start moving with inflation.

These SG&A costs seem pretty damn high to me. I mean, they’ve only got 600 employees — if we generously assume $150k average, that still leaves $100m of other cost. This is a bad thing insofar as it means management are not running a tight ship, but potentially also a good thing insofar as it means overheads could probably be reduced if times really did get tough, without impacting the business too much.

Balance Sheet

Dine is pretty leveraged. They have $1.18 billion of debt, on which they pay ~$72m of annual interest. $594m of the debt, due in June 2026, is at a fixed rate of only 4.7%. When they refinance this, the rate is likely to increase ~3%, which will result in an extra $18m in annual interest. This is the main reason the $80m I cite differs from estimates you will see elsewhere, e.g. that analyst Nick Setyan from earlier.

$90m is a lot of interest to pay on $190m of operating profit. Is it dangerous? Probably not — operating profit has been very steady, and even in covid it remained above $100m. It would take an extended period of pretty severe mismanagement to get it down to a level at which that interest starts looking like a real problem.

If the US gets the mother of all recessions, credit markets tighten to hell, and they’re not able to cut G&A, I could see it becoming a problem in the nearer future - but this feels like a <5% likelihood scenario to me.

Estimating Earning Power

EBITA: TTM results have been pretty rough — a lot of restaurants (not all) have been struggling, as the US consumer has become far more value-conscious in their dining habits due to the bout of inflation — but realistically, the US economy could be in far worse shape than it is now, so we’ll take the $192m of EBITA as “normalised”.

Less interest: As explained, interest expense is likely to jump to about $90m before too long, so PBT of $102m.

Adjusted for capex: Capex has historically run about $10 million lower than current depreciation, but I think they’ve underinvested in capex for a while now, so I won’t make an adjustment there.

Less tax: Over the last 10 years, Dine has on averaged paid a tax rate 1% higher than federal. I don’t want to make any assumptions about Trump reducing the corporate tax rate, so we’ll assume it remains at 21%. So 22% overall.

Equals owner earnings: That all leaves us with about $80m of earning power, putting the multiple at 5x, given the current $400m market cap. I think that $80m is a level they should be able to at least sustain.

A quick comparison

The closest competitor to Applebee’s is Chili’s, which is owned by Brinker ($EAT), and accounts for the vast majority of their sales. Brinker got a new CEO in June 2022, and since then the divergence in performance between $DIN and $EAT has been pretty astounding:

Why exactly has this happened?

To start with, I’d say the Chili’s brand is somewhat stronger than Applebee’s. However, from 2015-2021, their revenue barely grew at all, and profits actually halved. It was only when the new guy, Kevin Hochman, came in that things started looking up. Listen to this quote from a franchisee in NJ:

“We’ve just seen such a turnaround [under Hochman]... from the support we get from our bosses to the technology, the culinary innovations, all of those things. It made Chili’s fun again.”

This started having an effect pretty quickly. In the first year after Hochman joined, same-store sales grew 7%, compared to ~3% at Applebee’s. In the second, they clocked in 7.4%, versus just over 1% for Applebee’s.

But if you look at the chart above, you’ll notice it was really in the second half of 2024 that things started to get extreme. This was mostly due to social media. Partially it was their own doing — they have embraced social media and influencer marketing, for example always trying to reply to viral tweets with something witty. It’s not a coincidence this came after Hochman replaced their CMO shortly after joining. But also, their Triple Dippers meal went pretty viral on TikTok for some reason, causing an absolute flood of young people to the chain. That confluence of good management, good marketing and a heavy dose of luck has led to some pretty unprecedented performance: same-store sales in the most recent quarter are up 31% YoY. Profits in the last 6 months have tripled relative to a year prior.

I bring this up mostly just to highlight how much of a difference management can make. That’s not a bullish point for Dine, at least on the surface. But, it does bring up yet another potential catalyst — the possibility of a change of management. I would guess the board would only tolerate another year or two of poor performance relative to peers before deciding they’re fed up with Peyton. Of course, whoever replaces him in that scenario might not be much better — they could even be worse — but there’s at least a reasonable chance they can get someone actually worth their salt with the insane comp they seem happy to dish out.

(I think there’s another interesting angle here. Sure, Brinker’s TTM profits have doubled while Dine’s are flat — but the majority of the stock price divergence has come from changes in multiple. Dine’s P/E has fallen from ~12 to ~5, while Brinker’s has shot from ~10 to 27. Not only does the market seem to think this supranormal profitability is sustainable, it reckons the growth can continue. I’m not convinced that’s the right conclusion. I actually think this is a good example of something I’ve been thinking a lot about recently, which is that the market has a tendency to be overly deterministic, and to underestimate the impact of randomness. That shouldn’t come as a surprise, since it’s known to be an inherent human bias (see Naseem Taleb’s Fooled by Randomness) — but I wonder if there’s also an opportunity for alpha there. For example, if I was a long-short hedge fund, I might be looking at a short on Brinker as a short-term play (likely hedged with a long on Dine). But that’s not really my style.)

Conclusion

5x earnings is cheap. You don’t need me to tell you that. The question is, is that cheap enough to accept the shitty management and question marks around capital allocation?

I think it probably is. As it stands, it doesn’t seem like a Buffett-style “fat pitch” to me. But with those three embedded call options I discussed (multi-branded restaurants, major buyback programme, change of leadership), I reckon it makes sense as a small position. And if one of the above comes to fruition, and the market doesn’t react — that begins looking like a much fatter pitch.

Then again, I would not blame anyone for not joining me in this investment. I’m well aware I’m buying something Buffett probably wouldn’t. We’ll see whether that turns out to have been a very smart or very stupid decision.

And as always — not investment advice.

If you enjoyed this post and aren’t already subscribed, I reckon you should be. If you enjoyed it and are subscribed, I reckon you should share it with someone else. And in either case, you should definitely hit like — it’s the best way of letting Substack know I’m worth my salt. Thanks!!

This was a great piece. Management must be studying EAT turn around

Nice write-up!

I don't know if I'm not comfortable enough with high debt, or if you're too comfortable. But a Net Debt/EBITDA of 6.4 is quite something. Looking at it from an Enterprise Value perspective EV/EBITDA is 8, which doesn't seem super cheap for a no to low-growth story.

But with proper capital allocation I can see the appeal of the 20% yield.